The Future of Payments: SWIFT, TARGET2 and ISO 20022

The payments sector in Europe is undergoing a major upheaval. While banks are still busy implementing the Second Payment Services Directive (PSD2) and facing the challenges of open/digital banking, the growing customer demand for transparent, digital, cashless, and cross-border payments is simultaneously calling for a fundamental modernization of the payments’ infrastructure: The UNIFI standard (UNIversal Financial Industry message scheme), or ISO 20022, is set more and more into focus.

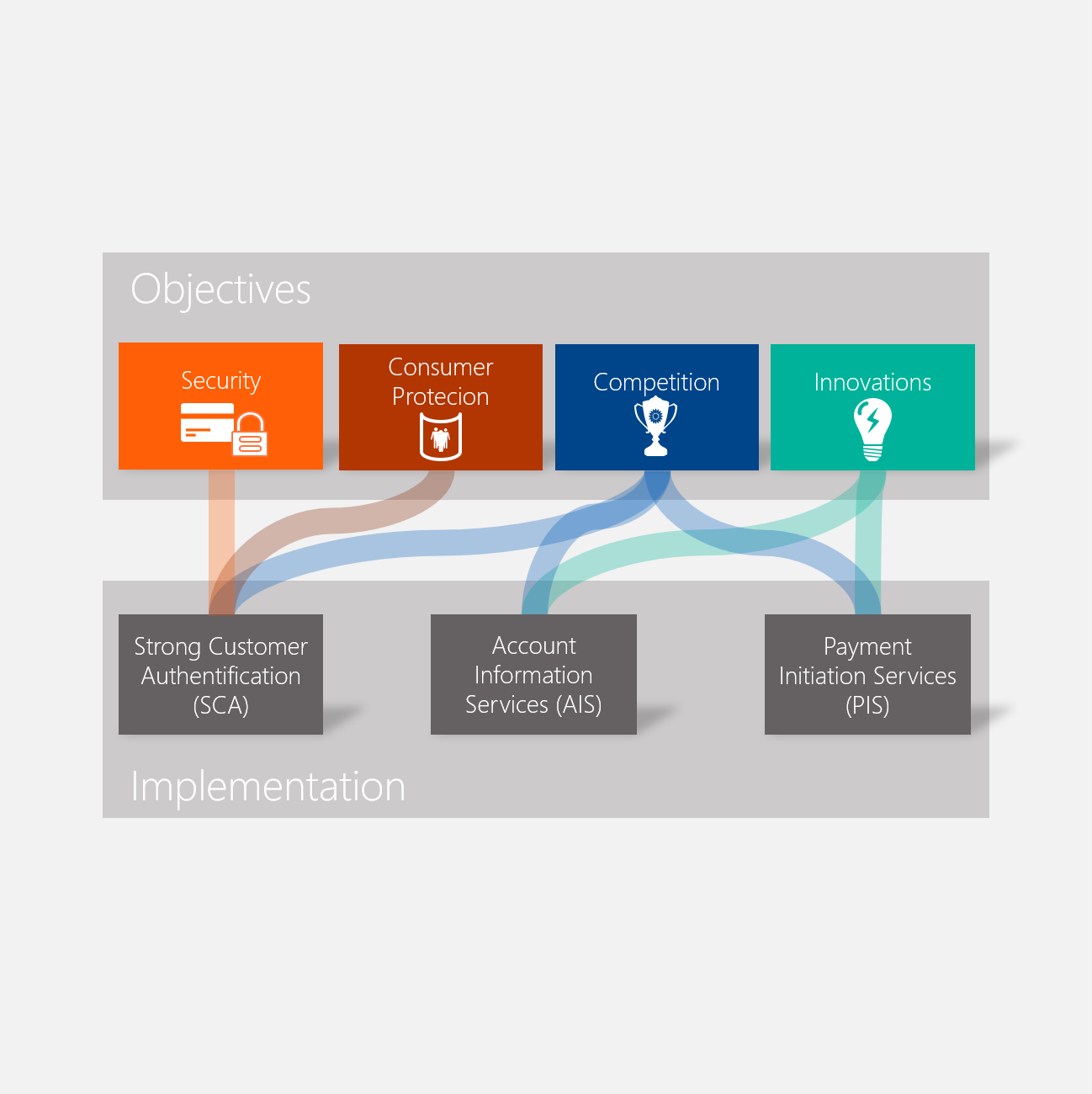

PSD2

The Payment Services Dircective 2 (PSD2) is the renewal of the EU Payment Services Directive that has entered into force on 14 September 2019. It obliges all banks in the EU to implement stronger security concepts (Strong Customer Authentication, SCA), to provide data on customers, their accounts and transactions to third party providers (Account Information Services, AIS) and to set up payment initiation services (PIS), which can be used by third parties to initiate transfers and transactions. This is achieved through the mandatory provision of APIs, that are accessible and usable for all market participants. More on PSD2

What began in 2014 with the launch of the European Payments Area (SEPA) is now being consistently pursued in the context of the consolidation of TARGET2 (Transeuropean Automated Real Gross settlement Express Transfer system) and the introduction of the Eurosystem Single Market Infrastructure Gateway (ESMIG) by the Eurosystem – the association of the Euro contries and the ECB. Over the next year and a half, all European large-value payment systems will be migrated to the international messaging standard, and also the most established financial messaging service provider SWIFT (Society for Worldwide Interbank Financial Telecommunication) joins in.

The European payments infrastructure will change fundamentally and open up enormous opportunities in terms of process efficiency and an optimized customer experience. Even though the integration of the standard is not mandatory from a regulatory perspective: To keep pace with international developments, extensive implementation projects lay ahead of European banks. In this article, we provide a brief overview of what is at stake and when the changes will take effect.

What does the current situation look like?

In each payment transaction, financial messages for the exchange of information between the involved parties form the core for the processing of payments. A common language and a suitable data format are therefore particularly important for a smooth payment process.

So far, however, the market is highly fragmented. Many different standards for financial messages have been established and are being used depending on the geographical location and business area, for instance UNIFI (ISO), MT (SWIFT) and FIN. Especially in the context of increasing cross-border payment traffic, the use of different standards increasingly encounters the players with more complex challenges in translating from system to system and updating and maintaining processes. The coexistence of different standards leads to a lack of interoperability, high costs, a structural risk of misinterpretation, and is an obstacle to the progressive and increasingly demanded automation of processes.

Open Banking

Open banking generally describes the opening of banks to third party providers, such as FinTechs or e-commerce companies. Complete digital networking via APIs makes it possible to exchange data with all potential players in the market and to offer financial services, even without owning a banking license. Open Banking is the concept of an integrated marketplace that creates specialized roles for each player and enables a seamless exchange of data and services. More on Open Banking

What is ISO 20022?

Already in 2004, the International Organization for Standardization –ISO for short – published its ISO 20022 standard for financial messages. The aim was to establish a globally uniform language for payment data, in order to harmonize the increasing number of cross-border payment transactions and improve communication between the players.

Based on the Extensible Markup Language Syntax (XML) – an open technical standard for electronic communication – the standard describes a logical data and information structure and, at the same time, offers a syntax-independent but commonly understood description of business processes and information needs. The standard also regulates the general flow of financial messages and processes for maintaining and developing these messages. Suggestions for additional messages can be submitted by all users to a central registry and added to the message catalog as an enhancement that is globally valid.

Meanwhile, ISO 20022 is not limited to the area of payment transactions anymore, but now also covers transactions in the securities business, foreign trade financing and treasury. Currently, the message compendium comprises about 750 business area components and more than 400 message definitions. ISO 20022 messages offer the full spectrum of payment transactions: customer-to-bank, bank-to-bank and reporting (cash management) [2].

Payment infrastructure

To process payments, several systems are necessary, whereas a distinction is made between intrabank and interbank payment transactions. Payments in intrabank transactions are usually settled via an in-house system, as is the case with the German Sparkassen network. For bilateral exchanges between two credit institutions, external clearing systems are often used, usually offered by central banks. In Europe, in addition to the Eurosystem, the EBA (European Banking Association), currently consisting of 48 banks from all over Europe, also offers privately operated clearing houses. In general, clearing systems for national and international payment transactions can be divided into three categories: large-value payment systems, mass payment systems for the processing of retail payments and the newly emerging real-time payment systems. The payment transaction data are exchanged via communication networks. For international payment transactions, for instance, the provider SWIFT (Society for Worldwide Interbank Financial Telecommunication) has established the most important one. SWIFT not only maintains the messaging network, but also, to date, its own standard for financial messages (MT standard).

What are the advantages and possibilities of ISO 20022?

The accelerating globalization and the associated need for interoperability and flexibility of the payments infrastructure are increasingly pushing the structures currently in use to their limits. On the one hand, new digitization initiatives and new customer solutions offered on the market promote the growing demand for faster and more transparent payment processing – preferably in real time. On the other hand, increasing regulatory requirements in payment transactions, e.g. for anti-money laundering (AML), terrorism financing (CFT) or sanction and embargo checks, also require faster processing of large data sets and render conversion/translation errors and limited information in message formats no longer acceptable [2].

A full conversion to the ISO 20022 message scheme will enable financial institutions to address these problems and benefit from the following advantages:

Higher process efficiency: The standardized and harmonized message format allows banks to provide more comprehensive payment data and enables fast digital reconciliation, as each part of the message can be clearly assigned to a business process. As a result, higher straight-through processing rates are achieved in payment processing.

More comprehensive data: Extensive data components can be embedded in the syntax in a standardized way. In this way, format enhancements that support additional functions, such as special requests, account management, direct debit mandates, or regulatory information, replace error-prone free text components as presently used in many messages.

Greater reliability: As a globally valid standard, the message format also manifests as the internationally “spoken” language of payments, which protects against loss of information through the translation of different message formats.

Lower costs: Costs for maintaining different processing systems for payment transaction data can be avoided. Cost-intensive processes for providing and checking data to peripheral systems (billing, account statements, archive systems) can also be reduced.

Digital Compliance: By standardizing message formats, AFC-relevant data (e.g. Embargo/Sanctions Screening, AML) can be embedded in the message format and automatically processed.

Figure 1: Relevant clearing systems in Germany and Europe.

What Changes?

In order to benefit from the above listed advantages, a full integration of all participants is necessary. Currently, there are still many different standards in use, whereby so far, SWIFT with its MT message format has established itself as the common standard for international payment transactions. In recent years, however, ISO 20022 has become increasingly accepted and brought a turnaround in the market.

One of the driving forces behind the establishment of the standard was the launch of the Single Euro Payments Area (SEPA) in 2014, which currently governs retail credit transfers and direct debits in the Euro Area. As a result of the most complex implementation project since the introduction of the Euro, the SEPA migration was worldwide the first introduction of an ISO 20022-compliant payment transaction messaging system for cross-border mass payment transactions. Currently, the standard is supported by the pan-European clearing system for SEPA mass payment transactions STEP2 and by the two real-time clearing systems TIPS and RT1, both established in 2018 [3][4].

While plans for the transition to the new message scheme are also evolving outside Europe, the Eurosystem has announced the transition of the next big chunk. Whereas until now, only mass payments and real-time credit transfers have been adapted to the message standard through SEPA, the two European large-value payment systems of the Eurosystem (TARGET2) and the European Banking Association (EBA) (EURO1) are now following suit.

As part of the consolidation of TARGET2 and the introduction of the European Single Market Infrastructure Gateway (ESMIG), the Eurosystem has decided to fully migrate to ISO 20022. The migration will be carried out in a "big bang", i.e. there will be no transition period. From 22nd of November 2021, the access to the TARGET2 system will only be possible via ISO 20022-conform communication channels [5]. Also, the EU’s only private large-value payment system, EBA Clearing's EURO1, which processes its payments through the TARGET system, will also migrate simultaneously from the FIN-based messaging system to ISO 20022 messages in order to ensure full intraday interchangeability between the two systems [6].

![Figure 2: Timeline of the ISO 20022 implementation of relevant market players. Sources: [8],[10],[11],[12],[13],[14]. *The US Fed has announced to pause and revise the current implementation plan [14]. ** According to the BoE, schedule is subject to…](https://images.squarespace-cdn.com/content/v1/54f9ea6be4b0251d5319ad8b/1584969982480-KM9SHSG3ZSTQ1NXHIJS3/Bild2_EN.png)

Figure 2: Timeline of the ISO 20022 implementation of relevant market players. Sources: [8],[10],[11],[12],[13],[14]. *The US Fed has announced to pause and revise the current implementation plan [14]. ** According to the BoE, schedule is subject to +- six months.

In addition, within ESMIG, communication channels to the Eurosystem's market infrastructures for all stakeholders, i.e. banks, central securities depositories, automated clearing houses (ACHs) and other payment service providers (PSPs) will be replaced by a single interface. In the course of this process, SWIFT, probably the most established provider that has been awarded a contract as messaging service provider for the interface, has also announced that it will make the new messaging standard available at the same time as the Eurosystem and EBA Clearing. In contrast to the Eurosystem's "big bang", however, SWIFT is offering a parallel phase in which the "old" MT standard is still supported. By the end of 2025, SWIFT will discontinue support for MT messages in categories 1, 2 (credit transfers) and 9 (cash management) [8].

What are the banks’ options?

For banks, the transition to ISO 20022 is not mandatory from a regulatory perspective. However, considering that the entire European payments infrastructure will be migrated to the new message standard from 2021 onwards, and that an estimated 87% of all large-value payments will be processed via ISO 20022 in 2025 [4], ignoring these developments entails considerable risks. At worst, banks could lose access to their central bank account and , which could negatively impact liquidity management. In addition to the business and operational risks involved in the settlement of payment transactions, no direct participation in monetary policy/ market operations can take place. If banks deter to migrate their systems to the message scheme, access must be realized either via another market participant (correspondent bank) or via conversion solutions that are error-prone and expensive.

In order to maintain barrier-free access to the TARGET system, banks should decide as soon as possible on one of the two network service providers approved for ESMIG, including SWIFT, and integrate their message protocols into their back-office processes. In general, banks can opt for a complete migration of their peripheral systems or rely on conversion solutions. However, since ISO 20022 messages offer more data and fields for information, it is not possible to translate messages one-to-one from other, previous formats. Conversion solutions not only bear the risk of misinformation, but also the loss of information through truncation of messages sent in old formats [4]. Even if the migration to ISO 20022 leads to enormous challenges for the banks, the upgrade of all payments linked systems should be planned considerately and started as early as possible.

Conclusions

Although the timetable for implementation is tight, there are benefits to be gained from a full transition to the ISO messaging standard, where banks can strengthen their position in the long term through cost efficiency and customer satisfaction. The market infrastructure will change radically in the coming years and banks should be prepared at an early stage. While mass and real-time payment systems in Europe are already using the ISO 20022 standard, the migration of TARGET2, EBA EURO1 and SWIFT will offer few viable opportunities to escape the ongoing migration of global payments to ISO 20022.

References:

[1] Bankenverband: „ISO 20022 im Überblick“, visited 03/09/2020. https://bankenverband.de/media/files/ISO-20022_im-ueberblick.pdf

[2] SWIFT Standard’s Team (2020): ISO 20022 for dummies: SWIFT 4th Limited Edition. West Sussex: John Wiley & Sons, Ltd..

[3] Deutsche Bank Global Transaction Banking: „Ultimate guide to ISO 20022 migration: Umfassender Leitfaden zur ISO 20022-Migration“, visited 03/09/2020. https://cib.db.com/docs_new/UltimateGuideGE.pdf

[4] Swift: “Brave New World ESMIG Paper 2019”, White paper, visited 03/09/2020. https://www.swift.com/resource/brave-new-world-be-ready-europes-new-payments-architecture

[5] ECB: “TARGET Annual Report 2018”, visited 03/09/2020. https://www.ecb.europa.eu/pub/targetar/html/ecb.targetar2018.en.html#toc8

[6] EBA Clearing: „Annual Report 2018“, visited 03/09/2020. https://www.ebaclearing.eu/media/azure/production/2204/eba-clearing-annual-report-2018_double-page-view.pdf

[7] ECB MIP news: “SIA-COLT and SWIFT bid to become ESMIG connectivity providers”, visited 03/09/2020. https://www.ecb.europa.eu/paym/intro/news/html/ecb.mipnews190408.en.html

[8] Swift ISO 20022 Einführungsplan, visited 03/10/2020. https://www.swift.com/standards/iso-20022-programme/timeline

[9] msg-gillardon: „ISO 20022 im Zahlungsverkehr“, aufgerufen am 09.03.2020. https://publikation.msg.group/publikationsarchiv/fachartikel/723-2019-02-msggillardon-news-iso-20022-im-zahlungsverkehr/file+&cd=2&hl=de&ct=clnk&gl=de

[10] ECB ISO 20022 Implementation Plan, visited 03/10/2020. https://www.ecb.europa.eu/paym/initiatives/shared/docs/0abea-t2-t2s-2018-10-09-tccg-overall-key-milestones-to-ensure-a-successful-big-bang-migration-in-november-2021.pdf

[11] EBA Clearing ISO 20022 Implementation Plan, visited 03/10/2020. https://www.ebaclearing.eu/news-and-events/media/press-releases/24-october-2018-eba-clearing-and-swift-kick-off-euro1-iso-20022-migration-for-november-2021/

[12] Fed ISO 20022 Implementation plan, visited 03/10/2020. https://www.frbservices.org/assets/resources/financial-services/fedwire-phase-1-iso-20022-presentation.pdf

[13] CHIPS ISO 20022 Implementation plan, visited 03/10/2020. https://www.theclearinghouse.org/-/media/new/tch/documents/payment-systems/chips_iso_20022_key_program_dates.pdf

[14] Bank of England ISO 20022 Implementation plan, visited 03/10/2020. https://www.bankofengland.co.uk/-/media/boe/files/payments/rtgs-renewal-programme/iso-20022/chaps-iso-20022-migration-draft-like-for-like-schemas-review

[15] Fed FAQ ISO 20022 Implementation plan, visited 03/10/2020. https://www.frbservices.org/resources/financial-services/wires/faq/iso-20022-implementation.html